Gross revenues, revenue sources, patients, and revenue benchmarking

Few reliable normative data exist when it comes to assessing your practice’s business metrics. This study, initiated by Phonak, provides a wealth of information that dispensing practice owners should find useful when benchmarking their business’ performance against the industry and practices of a similar size and type.

During 2011, Phonak Hearing Systems commissioned Customer Care Measurement and Consulting, LLC (CCMC) to conduct a nationwide survey of hearing professionals to establish basic industry metrics. Similar studies had been sponsored by Phonak in 2008, 2009, and 2010.

This benchmarking survey was designed to provide individual hearing practices with a tool they can use to compare their performance against industry standards. These industry benchmarks can be used as a basis for assessing and setting realistic, continuous, and fact-based improvement goals.

A Web-based survey methodology was utilized. Responses were collected in July and August 2011. There were 386 respondents to the 2011 survey. References to “2010 results” and “2009 results” reflect actual practice performance data for these years; references to “2011 study” and “2010 study” reflect practice characteristics/opinions in the years these studies were conducted (eg, “How many full-time and part-time office locations does the practice have?” asked in the 2011 study and referring to office locations in 2011).

A section in the digital edition of this article labeled Practice Characteristics and Performance Worksheet, provides a summary of norms for the total hearing industry. Included are several key productivity measures, such as revenue per professional hour, instruments dispensed per professional day, and revenue per instrument dispensed. Every practice should continuously track and seek to improve its performance on such key metrics relative to industry norms.

Hearing Practice Characteristics

The most common type of hearing practice in the United States was a single full-time location (59%), staffed by one hearing professional (Table 1). (Unless otherwise noted, when the term “professional” is used in this report, the designation means full-time licensed professional.) A total of 34% of practices were of this type. An additional 25% of practices had two or more professionals working at a single full-time location. About one-third (30%) of practices had multiple full-time locations. The primary difference between 2011 and 2010 was the composition of single full-time locations. The percentage of solo professional practices decreased by 7%, while there was a corresponding increase of 6% in practices with two or more professionals.

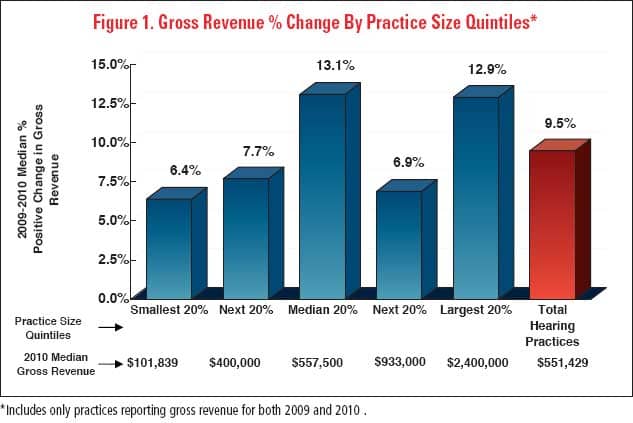

Gross revenues. The median hearing practice earned gross revenues of $551,429 during 2010 (Figure 1, bottom line in graph). The higher practice gross revenues reported by the top two quintiles can be explained by the higher revenues reported by the multi-full-time-unit and multi-professional practices. Median practice gross revenue growth during 2010 was +9.5%. Median and the largest sized practices enjoyed the highest rates of growth during 2010.

For single full-time-location/solo professional practices, the median 2010 gross revenue was $411,000 (Table 2). These offices were typically open 40 hours per week and the solo professional typically worked 2,000 hours annually (Table 3). Single full-time-location/solo professional practices had median office space of 1,000 square feet. They typically employed 3 non-hearing professional staff members.

Single full-time-location practices with two or more full-time professionals had median gross revenue of $740,000 during 2010—more than one and a half times the median of solo professional practices. Single full-time-location/2+ professional practices also were typically open 40 hours per week and had 2 full-time hearing professionals. The median square footage of these practices was 1,400. They typically employed 6 non-hearing professional staff members.

Multi-full-time-location practices had a median gross revenue of $1,441,266. The median number of full-time locations for these practices was three. The total median square footage of these practices was 2,800, and they employed a median of 10 non-hearing professional staff members.

Within each practice type, there was a considerable range of median gross revenue reported (Table 4). For example, among solo professional practices, the largest third of practices achieved a median gross revenue of $675,253—64% higher than the median for this type of practice. Multi-full-time-location practices in the top-third of that practice type had median revenue of $3.8 million and accounted for nearly 49% of the total revenue for all of the practices responding to the survey.

The median gross revenue per full-time hearing location was $477,833 during 2010. Among multi-full-time-location practices, the median gross revenue per location was $430,301, while the median gross revenue for a solo professional working at one location was $411,000. As would be expected, single full-time-location/2+ professional practices earned the most revenue per location—a median of $740,000.

The median gross revenue earned per hearing professional during 2010 was $375,000. Revenue reported per professional was highest in solo professional/single full-time location practices ($411,000), although revenue per professional for practices with multiple locations was only slightly lower ($405,000). The median revenue per professional for single full-time-location/2+ professional practices was much lower ($286,500).

Practice setting. A total of 40% of hearing practices identified themselves as private practice dispensers, while 26% said that they were a private practice audiologist or AuD. About one-fifth (21%) said that they worked in an ENT office; 10% in a medical institution (eg, hospital); 6% in a network affiliation; and 10% in other settings. Practices were able to select more than one response, and therefore there is some overlap between categories.

Staffing. For all hearing practices, there was a median of 2.5 non-hearing professional staff members per hearing professional (Table 3). The median for solo professional/single full-time-location practices was higher (a median of 3.0), while single full-time-location/2+ professional practices employed a median of 2.0 non-hearing professional staff members per professional. This suggests that staff is more efficiently deployed in single full-time-location/multi-professional practices.

Full-time hearing professionals outnumbered part-time professionals by 3 to 1 in hearing practices nationwide. Relatively few single full-time-location practices hired part-time professionals. Only 35% of single full-time-location practices hired part-time professionals, while 61% of multi-location practices hired part-time professionals.

A total of 16% of single full-time-location/solo professional practices employed one non-hearing professional staff member, 32% employed 2, 16% employed 3, and 36% employed 4 or more. All single full-time-location/2+ professional and multiple full-time-location practices employed at least 2 non-hearing professional staff. About one-third (32%) of single full-time-location/2+ professional practices employed 9 or more such staff, while just over half of multiple full-time-location practices employed 9 or more such staff.

Business hours. About two-thirds (64%) of the hearing practices were open between 36 and 45 hours per week, and 42% were open exactly 40 hours per week. Just 12% of the hearing practices were open more than 45 hours weekly; 24% were open 35 hours or less weekly. Practices with more than one professional were somewhat more likely to be open more than 40 hours weekly, but the median office hours for all practice types was 40.

Net profit. 2010 net profit was calculated by subtracting total practice expenses from gross revenue. The median net profit was $265,780 (Table 5). The top 20% of practices had a median net profit of $1,866,133. The bottom 20% had a median net loss of -$15,000. The net profit reported for the practice size quintiles likewise showed a very large gap between the smallest and largest practices. As would be expected, the net profit for multiple full-time-location practices was more than twice as high as the net profit for single full-time-location practices.

Sources of Revenue

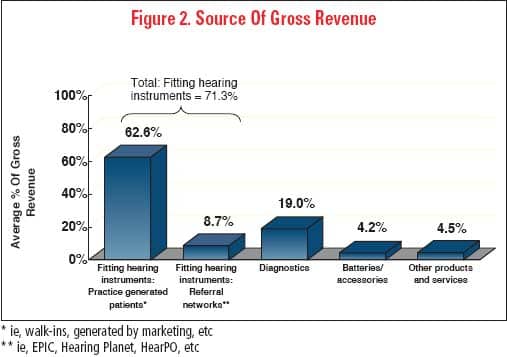

In US hearing care practices, revenue from fitting hearing instruments was an average of 71% of practice gross revenue during 2010 (Figure 2), compared to 75% in 2009. This category has been further broken down in Figure 2 into revenue from “practice generated patients” (62% of gross revenue) and revenue from “referral networks” (just under 9%).

Diagnostic testing contributed 19% to gross revenue for the average practice, compared to 15.3% in the 2009 survey. Source of revenue did not vary greatly by practice type or practice size. But size counts: practices in the largest quintile of this study earned more than 21 times the instrument fitting revenue as those in the smallest quintile.

Hearing Instruments Dispensed

Hearing care practices dispensed a median of 250 instruments during 2010 (Table 6, bottom) and a median of 210 instruments per full-time location (17.5 hearing aids per month), compared to a median of 225 instruments in 2009 (18.8 per month). Single full-time-location/solo professional practices dispensed a median of 176 instruments (14.7 per month). In the survey, multiple full-time-location practices dispensed a median of 450 instruments in 2010 (37.5 per month), a decrease from a median of 576 in 2009 (48.0 per month).

The median number of instruments dispensed per full-time hearing professional in 2010 was 152 (Table 7), or 12.7 hearing aids per month. Single full-time-location/solo professional offices achieved the highest dispensing rates per full-time professional—a median of 177 instruments dispensed per full-time professional (14.8 per month) versus 125 for single full-time-location/2+ professional practices (10.4 per month) and 153 for multiple full-time-location practices (12.8 per month).

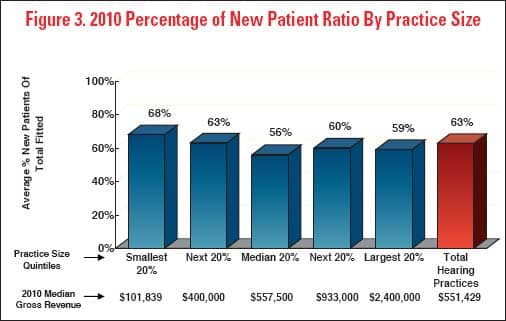

New patients. An average of 63% of instruments dispensed in 2010 were fit on patients new to the practice (Figure 3)—the exact same result as in 2009. The new patient ratio did not vary much by practice type or practice size. Practices with higher ratios of new patients tended to be smaller and at their current locations for fewer years. The respondents from these practices also tended to be newer audiology/dispensing licensees.

Productivity Benchmarks

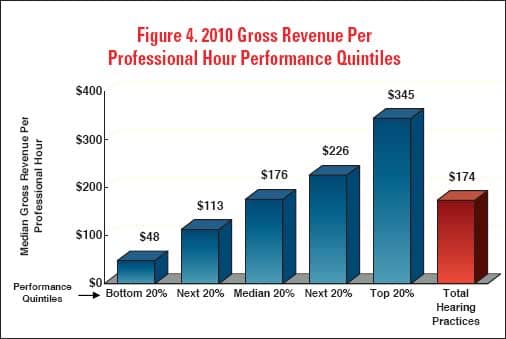

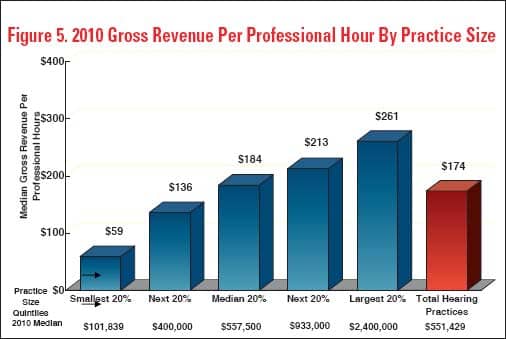

Gross revenue per professional hour. Gross revenue per professional hour is the most important productivity measure in dispensing practices. It reveals how effectively professionals use their time. It is calculated by dividing practice gross revenue by the total number of hours worked by all full-time and part-time hearing professionals for any specified period.

The median 2010 gross revenue per professional hour for all practices was $174 (Figure 4), compared to $144 in 2009. The most-productive 20% of practices achieved hourly professional revenue of $345—almost twice the median. The least-productive 20% of practices grossed just $48 per professional hour, 72% lower than the median and 86% lower than the most productive 20% of practices.

As would be expected, revenue per professional hour was lowest in the smallest 20% of practices (Figure 5). Moreover, these practices tended to be open fewer hours per week than larger practices; almost one-half of the smallest quintile of practices were open 35 hours or less per week versus just 18% of all other practices.

Multi-full-time-location practices reported the highest gross revenue per professional hour (Table 8). Professionals practicing in a single full-time location produced less revenue per hour.

Practices achieving the highest gross revenue per professional hour did so primarily by seeing more patients and therefore dispensing more instruments each day (Table 9). High production practices also fit instruments with somewhat higher-than-average fitting fees.

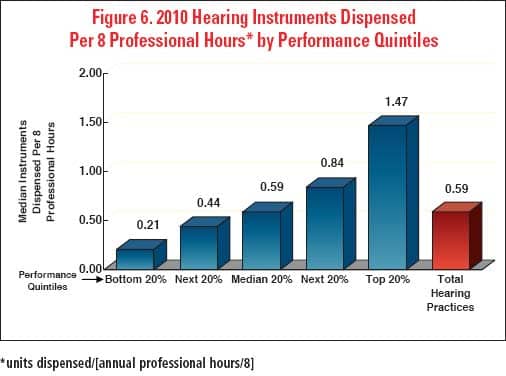

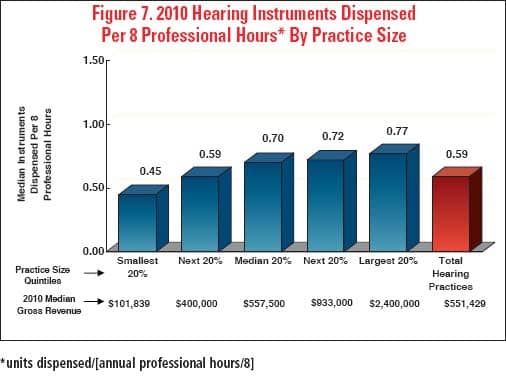

Instruments dispensed per 8 professional hours. A metric highly correlated with revenue per professional hour is instruments dispensed per professional day. The median practice fit 0.59 hearing instruments per 8 professional hours of work (Figure 6). Productivity varied widely across practices. The most-productive 20% of practices in 2010 fit 1.47 instruments per 8 hours. In contrast, the least-productive 20% in 2010 fit just one-seventh as many as the most productive quintile.

The largest sized practices reported the highest ratio of instruments dispensed per 8 professional hours of work (Figure 7). Practices with the highest ratio of units dispensed per professional day tend to be most successful in keeping their appointment calendars booked, unlike less successful practices that may have excess capacity.

Gross revenue per non-hearing professional staff member. The 2010 median gross revenue per non-hearing professional staff member was $132,474. The number of full-time professionals in a practice did not correlate with median gross revenue per non-hearing professional staff member, although practices with 3 full-time professionals generated the most revenue per non-hearing professional staff member.

2010 gross revenue per non-hearing professional staff member was not correlated with the number of such staff members that the practice employed. Practices with two non-hearing professional staff members reported a higher median gross ($200,000 per employee) than practices that had four or more non-hearing professionals ($127,714 per employee). Larger-size practices reported the highest median gross revenue per non-hearing professional staff member.

Practice gross revenue per instrument dispensed. The median gross practice revenue per instrument dispensed during 2010 was $2,143, compared to a 2009 median of $1,886. This ratio is affected both by the fees charged for instruments and by the percent of practice revenue produced by instrument fittings.

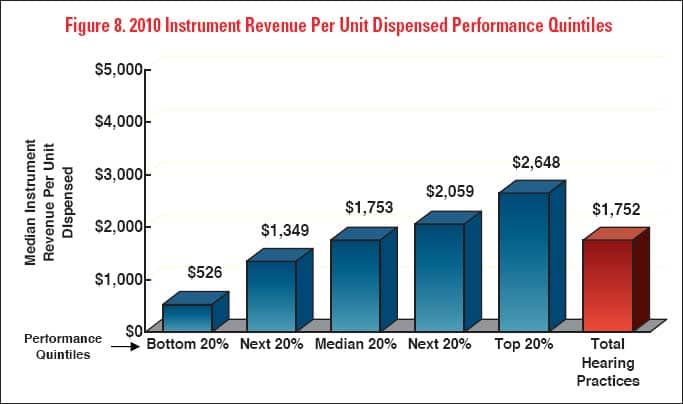

Instrument revenue (fees for both instruments and fittings) per unit dispensed. The median instrument revenue per unit dispensed in 2010 was $1,752 (Figure 8), compared to a 2009 median of $1,362. The 20% of practices achieving the highest instrument revenue per unit realized a median of $2,648 per unit fitted—51% higher than the overall median and 403% higher than practices in the lowest performance quintile.

Increased revenue per unit can be attributable both to a greater usage ratio of high-end technology, service offerings, and/or to higher mark-ups. Practices realizing the most instrument revenue per unit achieved a median gross profit margin of 66% compared to an overall median of 60%.

Performance benchmarks by practice type. Multi-full-time-location practices generated the highest revenue per professional hour (Table 10). Single full-time-location practices with more than one full-time hearing professional had somewhat lower performance on “gross revenue per professional hour,” “instruments dispensed per full-time professional,” and “hearing instruments dispensed per day.” Many of these practices may have attracted an insufficient number of patients to keep two full-time professionals busy. In other practices with two or more professionals, one of the professionals may have been spending considerable time on non-revenue producing administrative tasks that could have been more cost-effectively done by an audiology assistant, hearing aid tech, support staff member, and/or a more efficient office management system.

The Practice Performance Comparison worksheet (see the HR digital edition at: tinyurl.com/86sb4ua) shows instrument revenue earned per unit dispensed during 2010, based on the responses to the hearing industry survey. This metric is calculated using the formula: (2010 practice revenue x % of practice revenue from instrument dispensing)/number of instruments dispensed in 2010. You can perform this calculation yourself, as well as calculations of all the metrics discussed in this article.

Part 2 of this 2-part series will look at the types of hearing aids and fitting tests used, professional compensation, and practice marketing activities.

CORRESPONDENCE can be addressed to HR or Phonak Senior Manager of Marketing Kim Rawn at:

Citation for this article:

2011 Survey of US Dispensing Practice Metrics, Part 1. Hearing Review. 2012;19(08):16-23.